The main reason to stop trading N225 Index Option is : Tick Size!

What this means is :

- If the Option price is 50 points or less, the Option change price in 1 point up or down.

- Once the Option price goes over 50 points, the Option price change in 5 points up or down.

- And if the Option price goes over 1000 points (ie 1000 * JPY 1,000 = JPY 1,000,000), the Option price change in 10 points up or down. I have yet to encounter any Option price above 1000 points.

As an Options Seller, you want your Options to expire worthless. That is to say, you want your option price to go down. You do not want your option price to go up. You make money when option price goes down; you loss money when option price goes up.

Here is the problem of the Tick Size. When the option price goes down, below 50 points, it goes down 1 point at a time, slowly. When the option price goes up, over 50 points, it jump 5 points at time!

A typical premium collected from N225 Credit Spread is about 20 points. To reach the targeted profit of 80% (4 points), it goes down 1 point slowly from 20 to 4 points. However, when your option position goes against you, it will jump 5 points at a time. And 5 points is 25% of your collected premium!

At the point (Delta 25-30) that you need to make adjustment (or cut loss), your option price is definitely over 50 points. Your option price is definitely going to jump 5 points at a time. And because of the Difficulty In Trading Combo Order for K200 and N225 and the Problem In Combo Order Execution for K200 and N225, you will not just loss 5 points. You will loss 10 points due to the Bid/Ask Spread. That is 50% of your collected premium!

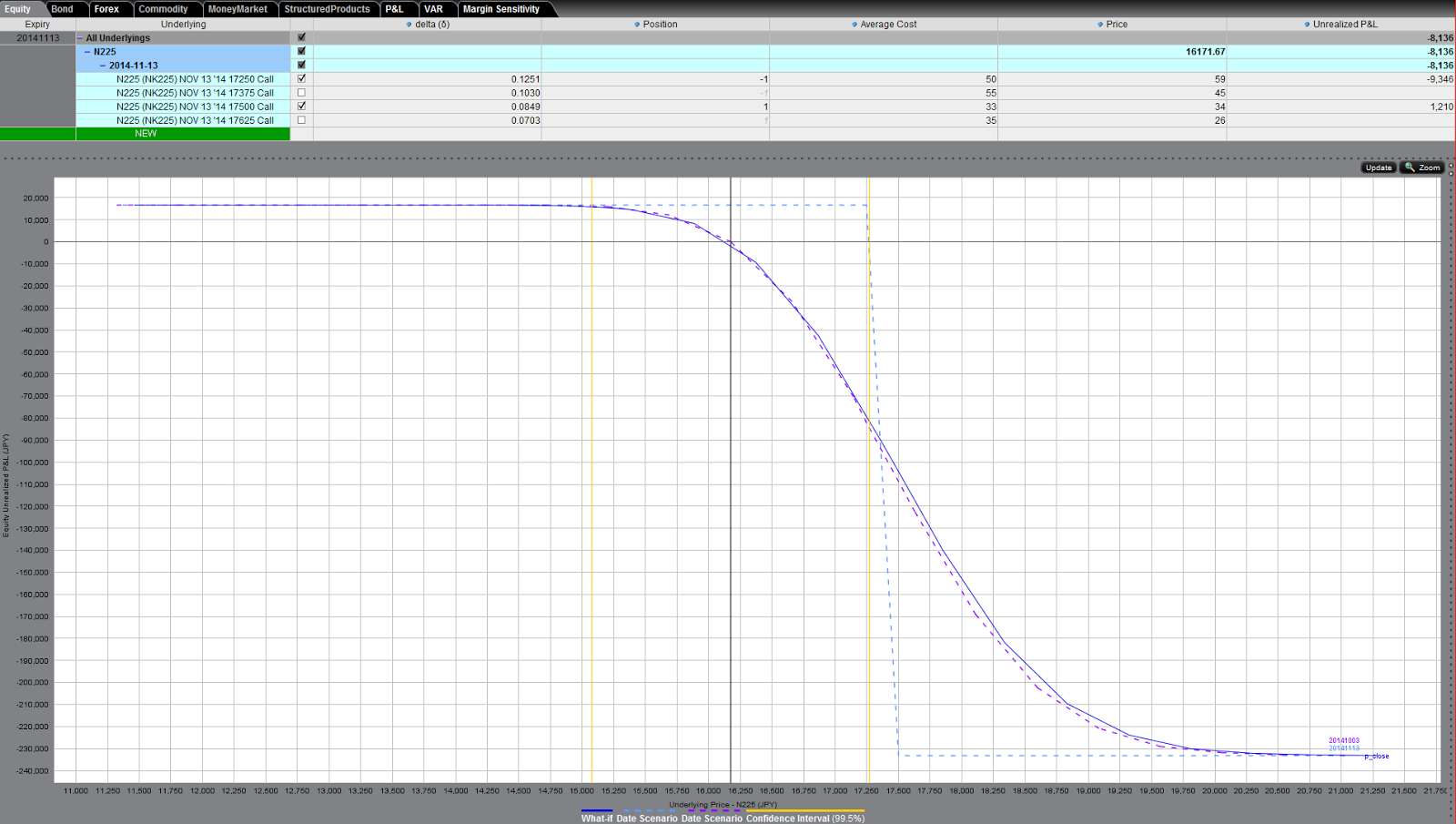

As you can see from the above screenshot, at Delta 14-23, the option prices are already above 50. With a tight Bid/Ask spread, you will see 5 point Bid/Ask spread at single option contract. With spread (due to two option contracts), the tight Bid/Ask spread is 10 points. The above screenshot didn't have the fortune of tight Bid/Ask spread, you ended up with 15 points Bid/Ask spread.

My analysis of my trade results show that I always end up losing more than 3X of the collected premium when I adjust (or cut loss) at Delta 25-30.

Even though Option Selling has higher probability (about 80%) of wining, you will still be hit with losing (even if it is 20% probability). Losing trade is certain. You will have to accept that you will have losing trade, about 1 out of 5. Hopefully 1 out of 10.

If you make 64 points in 4 wining trade (4 * 16 points = 64 points) but you loss 65-70 points (3 * 20 points + 5-10 points spread), you will end up losing even though you have higher probability of wining. This does not work.

The total wining must be more than the total losing. The lost trade has to be limit to about 2X, ie 40 points. With that, at least, you will end up wining 24 points (64 points - 40 points) for 1 losing trade out of 5 trades.

Therefore, here ends my option trading with N225. I will only trade K200 from May. I will start to explore commodity future option to diversify. I think trading with just one Index Option is a bit risky even though I know there are people simply trade S&P500 Index Option or Russel 2000 Index Option solely.

Well, let's continue to explore in this journey of Option Trading.