There is a way to address this unlimited risk by buying another Option with the same expiration and have the same underlying asset. That is a Vertical Spread.

A Vertical Spread is the simultaneous purchase and sale of options of the same class (calls or puts) and expiration, but with different strike prices.

By selling a Put at a higher price and buying another Put at lower price, it is called Bull Put Spread or Credit Put Spread. It is called Bull Put Spread strategy because it is a Bullish strategy. It is called Credit Put Spread because you will receive a positive cash flow or credit by executing this strategy.

Let's use a Example to compare and contrast Naked Put strategy with Bull Put Spread strategy.

ASML has been in a bullish uptrend throughout 2013. The recent weakness has sent the price retrace to price support at 92.30. Our Stop Loss is the last swing low support at 87.00

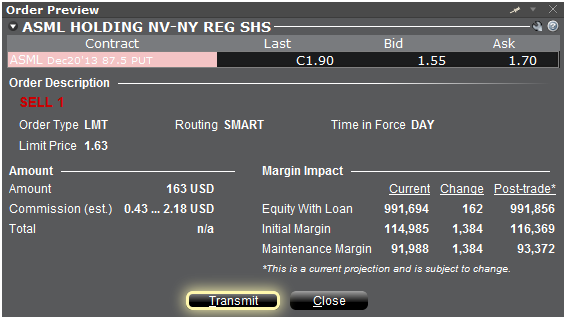

Selling Naked Put

There is no Strike Price at 87.00. There two nearest are 85.00 and 87.50. I therefore chose 87.50 Strike price with December Expiration : ASML Dec20'13 87.5 PUT.

I queue for mid point 1.63 (Bid is 1.55; Ask is 1.70). Didn't get it after 1 hour. Decided to just buy from Bid (ya, it dropped from 1.55 to 1.50). So, I received $150 (before commission) in premium.

With the margin of $1,384, the ROM (Return on Margin) is 150/1384 = 10.83% for 63 days.

Maximum loss is unlimited or price drop to 0, ie 87.50 * 1 * 100 - 150 = $8,600.

Vertical Spread : Bull Put Spread / Credit Put Spread

Components : Sell ASML Dec20'13 87.5 PUT

Buy ASML Dec20'13 85 PUT

As the premium for the spread is very low, just $24 for 1 contract at mid point $0.48. I have to increase to 5 contracts to have a comparable size with the Naked Put position.

Same as Nake Put trade, I queued at mid point $0.48 for 1 hour without filled. Decided to just take bid price 0.35. Therefore, premium collected is $175 (before commission).

Margin, however, is only $1,250 lower than Naked Put 1 contract margin. ROM is 175/1250 = 14%.

Maximum loss = (87.5 - 85) *5 * 100 - 175 = 1,075. (difference between strikes minus credit)

Summary:

Vertical Spread address the unlimited risk we have when selling Naked Put. In addition, it requires less margin and provide a better return on margin.

No comments:

Post a Comment